The mortgage market in Germany

Kop-Munt, Thursday, 10 August 2017

The German mortgage market is facing a complex period, with increasing competition and a smaller population eligible for a mortgage. The country is ageing rapidly. Of the more than 82 million inhabitants, 50 million are now in the age category 20-64. But in 13 years' time, in 2030, there will be only 34 million Germans left who are young enough to pay a mortgage.

Although Germany, after the United Kingdom, is the largest mortgage market in Europe, the German housing market operates differently from the rest of the EU. Germans feel, according to Ilse Helbrecht and Tim Geilenkeuser of the Humboldt University in Berlin, much less the need to own their own house than British, Italians or Spaniards. Only slightly more than half of the families own the house in which they live. According to figures from the European Mortgage Federation, the Netherlands accounts for around 67% of the population in the EU as a whole, and 70% throughout the EU. The main reasons for this are a large supply of affordable and high quality rental housing and a tax regime that does not favour homeowners over tenants. Some provinces have set up incentive schemes for first-time buyers, but these are small-scale.

Few homes for increasing demand

The German housing market is characterised by calm. Between 2003 and 2006, when housing markets were in the process of exploding in Europe - Spain, Greece and Ireland saw mortgage volumes rise between 132 and 153 per cent - mortgage loans increased by only 5.9 per cent in Germany, the lowest growth rate in the EU as a whole. And during the financial crisis, the mortgage market in Germany remained stable, as did the house prices, which showed little movement in previous years. Only this decade has both the prices of purchases and rents in Germany increased: since 2010, the average purchase price of a house has increased by 22 percent. According to analysts, Germany is building too few homes, while demand for housing is increasing. A small catch-up is expected in the coming years. Combined with historically low mortgage interest rates (around 1 percent for a loan with a Loan-to-value of less than 60 percent and a fixed-interest period of 10 years), this means that mortgage volumes can also show an increase. But mortgage providers will have to fight hard for that.

Greater role for independent consultant

The German mortgage market is strongly localised. Local savings banks are the most important player and own one third of the market. Cooperative banks account for a quarter of the market, as do the large banks. The German branch of ING has a market share of about 7 percent. Because the local savings banks are such a strong player, national mortgage lenders keep a close eye on what is happening in which region - even location-dependent interest rate rebates are granted to attract more customers. This works because the (independent) mortgage advisor is gaining ground. Germans traditionally stepped to their house bank to take out a mortgage, but are now looking around more and more. Analysts therefore expect competition to increase further. Advisors receive a fee from mortgage lenders, but they have to make this transparent to the client. Advisors who charge house buyers a fee for their services may not receive compensation from the lender.

Bausparen (Home savings)

Moreover, lenders in Germany are fairly strict: a typical Loan-to-value, as quantified by Humboldt University, is 67% and the cost of living should not normally exceed 25% of household income. A popular form of mortgage in Germany is the so-called' bausparen', where the consumer saves a number of years, up to half of the mortgage sum, before buying a house. The bank pays little interest on these savings, but also charges relatively little interest on the mortgage. As house buyers earn more, banks become more flexible in their terms and conditions. But Loan-to-values of more than 90 percent are exceptional. This is because, looking at past price trends, banks do not expect large price increases. This is also of less importance for the average house buyer itself. A house is a purchase for the rest of life, which is why Germans, like Dutch citizens, opt for a long-term fixed- interest period: more than two thirds fix the interest rate for five years or more, while a third choose ten years or more. Germans like security.

This article of is subject to a license. Based on . Translated from the Dutch language by Jos Deuling.

This article of is subject to a license. Based on . Translated from the Dutch language by Jos Deuling.

The German mortgage market is facing a complex period, with increasing competition and a smaller population eligible for a mortgage. The country is ageing rapidly. Of the more than 82 million inhabitants, 50 million are now in the age category 20-64. But in 13 years' time, in 2030, there will be only 34 million Germans left who are young enough to pay a mortgage.

Although Germany, after the United Kingdom, is the largest mortgage market in Europe, the German housing market operates differently from the rest of the EU. Germans feel, according to Ilse Helbrecht and Tim Geilenkeuser of the Humboldt University in Berlin, much less the need to own their own house than British, Italians or Spaniards. Only slightly more than half of the families own the house in which they live. According to figures from the European Mortgage Federation, the Netherlands accounts for around 67% of the population in the EU as a whole, and 70% throughout the EU. The main reasons for this are a large supply of affordable and high quality rental housing and a tax regime that does not favour homeowners over tenants. Some provinces have set up incentive schemes for first-time buyers, but these are small-scale.

Few homes for increasing demand

The German housing market is characterised by calm. Between 2003 and 2006, when housing markets were in the process of exploding in Europe - Spain, Greece and Ireland saw mortgage volumes rise between 132 and 153 per cent - mortgage loans increased by only 5.9 per cent in Germany, the lowest growth rate in the EU as a whole. And during the financial crisis, the mortgage market in Germany remained stable, as did the house prices, which showed little movement in previous years. Only this decade has both the prices of purchases and rents in Germany increased: since 2010, the average purchase price of a house has increased by 22 percent. According to analysts, Germany is building too few homes, while demand for housing is increasing. A small catch-up is expected in the coming years. Combined with historically low mortgage interest rates (around 1 percent for a loan with a Loan-to-value of less than 60 percent and a fixed-interest period of 10 years), this means that mortgage volumes can also show an increase. But mortgage providers will have to fight hard for that.

Greater role for independent consultant

The German mortgage market is strongly localised. Local savings banks are the most important player and own one third of the market. Cooperative banks account for a quarter of the market, as do the large banks. The German branch of ING has a market share of about 7 percent. Because the local savings banks are such a strong player, national mortgage lenders keep a close eye on what is happening in which region - even location-dependent interest rate rebates are granted to attract more customers. This works because the (independent) mortgage advisor is gaining ground. Germans traditionally stepped to their house bank to take out a mortgage, but are now looking around more and more. Analysts therefore expect competition to increase further. Advisors receive a fee from mortgage lenders, but they have to make this transparent to the client. Advisors who charge house buyers a fee for their services may not receive compensation from the lender.

Bausparen (Home savings)

Moreover, lenders in Germany are fairly strict: a typical Loan-to-value, as quantified by Humboldt University, is 67% and the cost of living should not normally exceed 25% of household income. A popular form of mortgage in Germany is the so-called' bausparen', where the consumer saves a number of years, up to half of the mortgage sum, before buying a house. The bank pays little interest on these savings, but also charges relatively little interest on the mortgage. As house buyers earn more, banks become more flexible in their terms and conditions. But Loan-to-values of more than 90 percent are exceptional. This is because, looking at past price trends, banks do not expect large price increases. This is also of less importance for the average house buyer itself. A house is a purchase for the rest of life, which is why Germans, like Dutch citizens, opt for a long-term fixed- interest period: more than two thirds fix the interest rate for five years or more, while a third choose ten years or more. Germans like security.

This article of is subject to a license. Based on . Translated from the Dutch language by Jos Deuling.

Search for German property and real estate for sale in all regions of Germany. Villas, appartments andfarmhouses for sale in Berlin, Rhineland-Palatinate and Saxony

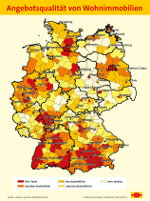

If you look at the quality of the housing stock in Germany there is a clear East-West divide. This emerges from a study of the German building society

Schwäbisch Hall. The market research firm Empirica has evaluated approximately 743,000 homes in Germany. The data are displayed by region on a map

of Germany.

If you look at the quality of the housing stock in Germany there is a clear East-West divide. This emerges from a study of the German building society

Schwäbisch Hall. The market research firm Empirica has evaluated approximately 743,000 homes in Germany. The data are displayed by region on a map

of Germany.